SURFING THE WEB FROM INSIDE YOUR CAR

Accessing email from your Blackberry or iPhone is soon to become only the most basic of high-tech activities for the car-bound commuter.

According to John R. Quain of the New York Times, major cellphone carriers such as AT&T, Verizon and Sprint now offer unlimited monthly subscriptions to high-speed wireless data services. Just slide the wireless data PC card into your laptop and you're on!

Granted, the picture quality for on-line video technologies is not the same as your cable connection, and the strength of the wireless signal depends on your proximity to the carrier's cellphone towers. Still, the technology can only get better.

Just remember to leave the web surfing to the passengers. Someone needs to get us there safely!

To read the entire article, with pricing and product details, click here.

Tuesday, November 27, 2007

Saturday, November 24, 2007

2008 California Market Forecast & Statistics Galore!

That's right! On October 10, California Association of Realtor (CAR)'s Vice President and Chief Economist, Leslie Appleton-Young, released the 2008 Real Estate Market Forecast for all of California.

Click HERE to access regional and state-wide statistics, detailed charts and graphs, a 2008 forecast and 2008 market opportunities!

For more information on taking advantage of this forecast and more, be sure to call me at 831-457-5550 or shoot me an email at frank@frankmurphy.net!

That's right! On October 10, California Association of Realtor (CAR)'s Vice President and Chief Economist, Leslie Appleton-Young, released the 2008 Real Estate Market Forecast for all of California.

Click HERE to access regional and state-wide statistics, detailed charts and graphs, a 2008 forecast and 2008 market opportunities!

For more information on taking advantage of this forecast and more, be sure to call me at 831-457-5550 or shoot me an email at frank@frankmurphy.net!

Thursday, November 08, 2007

Pin The Tail On The Bottom Of The Market!

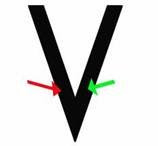

All of us Realtors have been working with would be home buyers here in Santa Cruz. It seems all of them feel that they should wait until the housing market is at the bottom before they buy a home. Let’s look at an interesting take on "the bottom of the market" and how it will effect your buying decision....

This is a graph that represents the Santa Cruz housing market. The left side of the V represents the market going down, the right side represents the market going up, and of course the bottom of the V represents the bottom of the housing market.

If I asked you to plot on this

graph where you thought the housing market

was right now ...

... would you pick this spot or something close?

So you think that the market is going towards the bottom. If the market isn't at the bottom yet, how will you know when it does hit the bottom?

How will you know when the housing market hits the bottom?

Experience tells us you won't know that the housing market has hit the bottom until prices start to go back up. It will be difficult to be sure that the market has hit bottom for a few months. It’s not a sudden shift, it’s a gradual shift. You'll be able to tell that the market has turned when prices reach this point (green arrow).

What is the difference in housing prices between the red arrow and the green arrow?

Not much... but there is another difference: a major difference.

If you buy a home on the left side of the graph, it is considered a buyers market. You would be more likely to get concessions from a seller including price reductions, repairs, upgrades, closing costs, maybe even personal property.

If you wait until the market turns and you buy on the upswing, you and every other buyer that has been waiting for the market to hit bottom will be bidding on the same house.

There really is no better time to buy a house than now, and here are some reasons why:

All of us Realtors have been working with would be home buyers here in Santa Cruz. It seems all of them feel that they should wait until the housing market is at the bottom before they buy a home. Let’s look at an interesting take on "the bottom of the market" and how it will effect your buying decision....

{kind=link}

This is a graph that represents the Santa Cruz housing market. The left side of the V represents the market going down, the right side represents the market going up, and of course the bottom of the V represents the bottom of the housing market.

If I asked you to plot on this

graph where you thought the housing market

was right now ...

... would you pick this spot or something close?

So you think that the market is going towards the bottom. If the market isn't at the bottom yet, how will you know when it does hit the bottom?

How will you know when the housing market hits the bottom?

Experience tells us you won't know that the housing market has hit the bottom until prices start to go back up. It will be difficult to be sure that the market has hit bottom for a few months. It’s not a sudden shift, it’s a gradual shift. You'll be able to tell that the market has turned when prices reach this point (green arrow).

{kind=link}

What is the difference in housing prices between the red arrow and the green arrow?

Not much... but there is another difference: a major difference.

If you buy a home on the left side of the graph, it is considered a buyers market. You would be more likely to get concessions from a seller including price reductions, repairs, upgrades, closing costs, maybe even personal property.

If you wait until the market turns and you buy on the upswing, you and every other buyer that has been waiting for the market to hit bottom will be bidding on the same house.

There really is no better time to buy a house than now, and here are some reasons why:

- There is a wonderful selection of homes to choose from right now.

- Sellers are very willing to negotiate on price, terms and perks.

- Interest rates are still at a historical low.

I'm suggesting we take a good look at the above examples and decide what percentage the prices will have to drop before a buyer thinks housing prices have hit bottom, and then offer that price. For example, if you think that prices will go down another 5%, then submit an offer at 5% below the asking price. Sellers will either counter, accept or decline. Then look at a loan payment based on current low interest rates. On an $875,000 home with an accepted offer 5% below asking, you'd end up at $831,250. Putting 20% down ($166,250) your loan would be $665,000. At 6% payments would run $3,325. If interest rates were to go up only half a point to 6.5%, the same home with the same $166,250 down would have to sell for $797,000 to end up with a similar loan payment.

The message here is to take advantage of the market today! Opportunity is knocking now!

Thursday, November 01, 2007

Fed Cuts Interest Rates by A Quarter Point

Interest rates have indeed been cut again, moving down from 4.75% to 4.5%.

While the cut was expected, it is now thought to be unlikely that rates will be cut again for quite sometime.

Fed Chairman Ben Bernanke was forced to make a decision in light of both a "faster-than-expected" growth in the economy and the threat of falling home prices and a falling dollar. And now, of course, the argument arises over whether Bernanke and the Fed are truly able to keep inflation under control.

To read about the Fed's decision in more detail and the controversy that surrounds it, go to the Wall Street Journal's article: Fed's Rate Cut Could Be Last For a While

Interest rates have indeed been cut again, moving down from 4.75% to 4.5%.

While the cut was expected, it is now thought to be unlikely that rates will be cut again for quite sometime.

Fed Chairman Ben Bernanke was forced to make a decision in light of both a "faster-than-expected" growth in the economy and the threat of falling home prices and a falling dollar. And now, of course, the argument arises over whether Bernanke and the Fed are truly able to keep inflation under control.

To read about the Fed's decision in more detail and the controversy that surrounds it, go to the Wall Street Journal's article: Fed's Rate Cut Could Be Last For a While

Subscribe to:

Posts (Atom)