TAX BREAK FOR MORTGAGE DEBT FORGIVENESS

President Bush signed into law today a new measure giving tax breaks to homeowners who have mortgage debt forgiven. Under preexisting law, the debt forgiven by a lender, such as for short sales and refinances, was generally taxable to the borrower as debt discharge income. With the passage of the Mortgage Forgiveness Debt Relief Act of 2007, a taxpayer does not have to pay federal income tax on debt forgiven for a loan secured by a qualified principal residence.

This tax break applies to debts discharged from January 1, 2007 to December 31, 2009. Qualified principal residence indebtedness is debt incurred in acquiring, constructing, or substantially improving the residence (up to $2 million for refinances).

For purposes of calculating capital gains, any debts discharged excluded from income under the new law must be subtracted from the basis of the taxpayer's principal residence (but not below zero). However, taxpayers may generally exclude from capital gains income up to $250,000 (or $500,000 for married couples filing jointly) for properties owned and used as their principal residence for at least two of the last five years.

For a copy of the Mortgage Forgiveness Debt Relief Act of 2007, go to http://www.govtrack.us/congress/bill.xpd?bill=h110-3648.

Brought to you by the CALIFORNIA ASSOCIATION OF REALTORS®

Friday, December 21, 2007

Thursday, December 20, 2007

MIT PHYSICS LECTURES AND MUCH MORE, FREE ONLINE!

Did you know about the free on-line lectures available from the Massachusetts Institute of Technology's OpenCourseWare program? Go take a look!

Click here to read Sara Rimer's article in the New York Times about Walter H. G. Lewin, one special physics professor who's "now emerged as an international Internet guru thanks to the global classroom."

Did you know about the free on-line lectures available from the Massachusetts Institute of Technology's OpenCourseWare program? Go take a look!

Click here to read Sara Rimer's article in the New York Times about Walter H. G. Lewin, one special physics professor who's "now emerged as an international Internet guru thanks to the global classroom."

Wednesday, December 19, 2007

Enjoy this video of the Indiana University men's a cappella group Straight No Chaser doing a special holiday medley!

Enjoy this video of the Indiana University men's a cappella group Straight No Chaser doing a special holiday medley!Tuesday, December 18, 2007

THE COST OF STAND-BY POWER

Ever wonder exactly how much power is actually being used by appliances "that are always 'on' while seemingly 'off'," such as a television?

C. CLAIBORNE RAY of the New York Times has the answer right here, including a laboratory Web site of Standby Power Data that "provides tables of the minimum, average and maximum power used by appliances that cannot be switched off completely without being unplugged."

Ever wonder exactly how much power is actually being used by appliances "that are always 'on' while seemingly 'off'," such as a television?

C. CLAIBORNE RAY of the New York Times has the answer right here, including a laboratory Web site of Standby Power Data that "provides tables of the minimum, average and maximum power used by appliances that cannot be switched off completely without being unplugged."

Tuesday, December 11, 2007

BEN STEIN'S "LESSONS FROM THE PITS"

Click here to read some of his thoughts on travel, investment, spending, and heroism--all with a good dose of his usual wit, of course.

When he isn't giving away his own money on Comedy Central or lending his talent to making memorable characters on the Big Screen, lawyer and economist Ben Stein has some pretty wise things to say about life.

Click here to read some of his thoughts on travel, investment, spending, and heroism--all with a good dose of his usual wit, of course.

Monday, December 10, 2007

The 53 Places To Go In 2008!

The 53 Places To Go In 2008!"What’s on your travel itinerary in the new year?"

From Laos to Hvar to Death Valley to Mozambique, click here to see beautiful photos from around the world and find out which destinations made the list!

From Laos to Hvar to Death Valley to Mozambique, click here to see beautiful photos from around the world and find out which destinations made the list!

List compiled by Denny Lee, courtesy of the New York Times.

Tuesday, December 04, 2007

INFORMATION FOR TAXPAYERS IN FORECLOSURE

Provided courtesy of the Internal Revenue Service

The IRS has developed information and Web resources to assist taxpayers with the tax issues presented by foreclosure.

Key Points:

*The Internal Revenue Service unveiled a special new section on www.IRS.gov for people who have lost their homes due to foreclosure.

*The IRS also reassured homeowners that although mortgage workouts and foreclosures can have tax consequences, special relief provisions can often reduce or eliminate the tax bite for financially strapped borrowers who lose their homes.

Resources:

*IRS 2007-159 – The news release IR 2007-159 provides additional background. The

news release and FAQs can also be found at http://www.irs.gov/newsroom/article/0,,id=174022,00.html

The direct link to the FAQ’s is http://www.irs.gov/newsroom/article/0,,id=174034,00.html

Provided courtesy of the Internal Revenue Service

The IRS has developed information and Web resources to assist taxpayers with the tax issues presented by foreclosure.

Key Points:

*The Internal Revenue Service unveiled a special new section on www.IRS.gov for people who have lost their homes due to foreclosure.

*The IRS also reassured homeowners that although mortgage workouts and foreclosures can have tax consequences, special relief provisions can often reduce or eliminate the tax bite for financially strapped borrowers who lose their homes.

Resources:

*IRS 2007-159 – The news release IR 2007-159 provides additional background. The

news release and FAQs can also be found at http://www.irs.gov/newsroom/article/0,,id=174022,00.html

The direct link to the FAQ’s is http://www.irs.gov/newsroom/article/0,,id=174034,00.html

Tuesday, November 27, 2007

SURFING THE WEB FROM INSIDE YOUR CAR

Accessing email from your Blackberry or iPhone is soon to become only the most basic of high-tech activities for the car-bound commuter.

According to John R. Quain of the New York Times, major cellphone carriers such as AT&T, Verizon and Sprint now offer unlimited monthly subscriptions to high-speed wireless data services. Just slide the wireless data PC card into your laptop and you're on!

Granted, the picture quality for on-line video technologies is not the same as your cable connection, and the strength of the wireless signal depends on your proximity to the carrier's cellphone towers. Still, the technology can only get better.

Just remember to leave the web surfing to the passengers. Someone needs to get us there safely!

To read the entire article, with pricing and product details, click here.

Accessing email from your Blackberry or iPhone is soon to become only the most basic of high-tech activities for the car-bound commuter.

According to John R. Quain of the New York Times, major cellphone carriers such as AT&T, Verizon and Sprint now offer unlimited monthly subscriptions to high-speed wireless data services. Just slide the wireless data PC card into your laptop and you're on!

Granted, the picture quality for on-line video technologies is not the same as your cable connection, and the strength of the wireless signal depends on your proximity to the carrier's cellphone towers. Still, the technology can only get better.

Just remember to leave the web surfing to the passengers. Someone needs to get us there safely!

To read the entire article, with pricing and product details, click here.

Saturday, November 24, 2007

2008 California Market Forecast & Statistics Galore!

That's right! On October 10, California Association of Realtor (CAR)'s Vice President and Chief Economist, Leslie Appleton-Young, released the 2008 Real Estate Market Forecast for all of California.

Click HERE to access regional and state-wide statistics, detailed charts and graphs, a 2008 forecast and 2008 market opportunities!

For more information on taking advantage of this forecast and more, be sure to call me at 831-457-5550 or shoot me an email at frank@frankmurphy.net!

That's right! On October 10, California Association of Realtor (CAR)'s Vice President and Chief Economist, Leslie Appleton-Young, released the 2008 Real Estate Market Forecast for all of California.

Click HERE to access regional and state-wide statistics, detailed charts and graphs, a 2008 forecast and 2008 market opportunities!

For more information on taking advantage of this forecast and more, be sure to call me at 831-457-5550 or shoot me an email at frank@frankmurphy.net!

Thursday, November 08, 2007

Pin The Tail On The Bottom Of The Market!

All of us Realtors have been working with would be home buyers here in Santa Cruz. It seems all of them feel that they should wait until the housing market is at the bottom before they buy a home. Let’s look at an interesting take on "the bottom of the market" and how it will effect your buying decision....

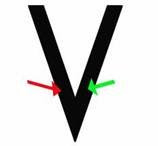

This is a graph that represents the Santa Cruz housing market. The left side of the V represents the market going down, the right side represents the market going up, and of course the bottom of the V represents the bottom of the housing market.

If I asked you to plot on this

graph where you thought the housing market

was right now ...

... would you pick this spot or something close?

So you think that the market is going towards the bottom. If the market isn't at the bottom yet, how will you know when it does hit the bottom?

How will you know when the housing market hits the bottom?

Experience tells us you won't know that the housing market has hit the bottom until prices start to go back up. It will be difficult to be sure that the market has hit bottom for a few months. It’s not a sudden shift, it’s a gradual shift. You'll be able to tell that the market has turned when prices reach this point (green arrow).

What is the difference in housing prices between the red arrow and the green arrow?

Not much... but there is another difference: a major difference.

If you buy a home on the left side of the graph, it is considered a buyers market. You would be more likely to get concessions from a seller including price reductions, repairs, upgrades, closing costs, maybe even personal property.

If you wait until the market turns and you buy on the upswing, you and every other buyer that has been waiting for the market to hit bottom will be bidding on the same house.

There really is no better time to buy a house than now, and here are some reasons why:

All of us Realtors have been working with would be home buyers here in Santa Cruz. It seems all of them feel that they should wait until the housing market is at the bottom before they buy a home. Let’s look at an interesting take on "the bottom of the market" and how it will effect your buying decision....

This is a graph that represents the Santa Cruz housing market. The left side of the V represents the market going down, the right side represents the market going up, and of course the bottom of the V represents the bottom of the housing market.

If I asked you to plot on this

graph where you thought the housing market

was right now ...

... would you pick this spot or something close?

So you think that the market is going towards the bottom. If the market isn't at the bottom yet, how will you know when it does hit the bottom?

How will you know when the housing market hits the bottom?

Experience tells us you won't know that the housing market has hit the bottom until prices start to go back up. It will be difficult to be sure that the market has hit bottom for a few months. It’s not a sudden shift, it’s a gradual shift. You'll be able to tell that the market has turned when prices reach this point (green arrow).

What is the difference in housing prices between the red arrow and the green arrow?

Not much... but there is another difference: a major difference.

If you buy a home on the left side of the graph, it is considered a buyers market. You would be more likely to get concessions from a seller including price reductions, repairs, upgrades, closing costs, maybe even personal property.

If you wait until the market turns and you buy on the upswing, you and every other buyer that has been waiting for the market to hit bottom will be bidding on the same house.

There really is no better time to buy a house than now, and here are some reasons why:

- There is a wonderful selection of homes to choose from right now.

- Sellers are very willing to negotiate on price, terms and perks.

- Interest rates are still at a historical low.

I'm suggesting we take a good look at the above examples and decide what percentage the prices will have to drop before a buyer thinks housing prices have hit bottom, and then offer that price. For example, if you think that prices will go down another 5%, then submit an offer at 5% below the asking price. Sellers will either counter, accept or decline. Then look at a loan payment based on current low interest rates. On an $875,000 home with an accepted offer 5% below asking, you'd end up at $831,250. Putting 20% down ($166,250) your loan would be $665,000. At 6% payments would run $3,325. If interest rates were to go up only half a point to 6.5%, the same home with the same $166,250 down would have to sell for $797,000 to end up with a similar loan payment.

The message here is to take advantage of the market today! Opportunity is knocking now!

Thursday, November 01, 2007

Fed Cuts Interest Rates by A Quarter Point

Interest rates have indeed been cut again, moving down from 4.75% to 4.5%.

While the cut was expected, it is now thought to be unlikely that rates will be cut again for quite sometime.

Fed Chairman Ben Bernanke was forced to make a decision in light of both a "faster-than-expected" growth in the economy and the threat of falling home prices and a falling dollar. And now, of course, the argument arises over whether Bernanke and the Fed are truly able to keep inflation under control.

To read about the Fed's decision in more detail and the controversy that surrounds it, go to the Wall Street Journal's article: Fed's Rate Cut Could Be Last For a While

Interest rates have indeed been cut again, moving down from 4.75% to 4.5%.

While the cut was expected, it is now thought to be unlikely that rates will be cut again for quite sometime.

Fed Chairman Ben Bernanke was forced to make a decision in light of both a "faster-than-expected" growth in the economy and the threat of falling home prices and a falling dollar. And now, of course, the argument arises over whether Bernanke and the Fed are truly able to keep inflation under control.

To read about the Fed's decision in more detail and the controversy that surrounds it, go to the Wall Street Journal's article: Fed's Rate Cut Could Be Last For a While

Tuesday, October 30, 2007

24-Hour Hotline Available to Help Avoid Foreclosure

According to Sentinel Staff Writer Jondi Gumz, "A national survey released Monday by the AFL-CIO reports that 49 percent of homeowners with adjustable rate mortgages admit they do not know how their mortgage adjusts and 73 percent do not know how much their mortgage payment will be after the adjustment.

"'This survey shows that many homeowners simply are not prepared for the steep rise in mortgage payments that this market inflicts on ARM [adjustable-rate mortgage] holders,' said AFL-CIO President John Sweeney.

"To help union members, their parents and their children who are trying to avoid foreclosure, AFL-CIO officials have opened a 24-hour hotline staffed by Money Management International, a HUD-certified counseling agency."

The "Save My Home" hotline is at 1-866-490-5361

To read Jondi's article in its entirety, go to Union Homeowners Know Too Little About Their Mortgage Payment

According to Sentinel Staff Writer Jondi Gumz, "A national survey released Monday by the AFL-CIO reports that 49 percent of homeowners with adjustable rate mortgages admit they do not know how their mortgage adjusts and 73 percent do not know how much their mortgage payment will be after the adjustment.

"'This survey shows that many homeowners simply are not prepared for the steep rise in mortgage payments that this market inflicts on ARM [adjustable-rate mortgage] holders,' said AFL-CIO President John Sweeney.

"To help union members, their parents and their children who are trying to avoid foreclosure, AFL-CIO officials have opened a 24-hour hotline staffed by Money Management International, a HUD-certified counseling agency."

The "Save My Home" hotline is at 1-866-490-5361

To read Jondi's article in its entirety, go to Union Homeowners Know Too Little About Their Mortgage Payment

Tuesday, October 02, 2007

WHY YOU SHOULD PRICE YOUR HOME REALISTICALLY

TIME Chances are that your home will sell at its fair market value. Pricing it realistically at the outset simply increases the likelihood of a timely sale with less inconvenience and greater monetary return.

COMPETITION Buyers educate themselves by viewing many homes. They know what is a fair price. If your home is not competitive in value with those they have already seen, it will not sell. Buyers typically look at homes within a $10,000 price range. If your home is not priced within the correct range, it very likely will not be exposed to its potential or targeted buyers.

REPUTATION Overpricing causes most homes to remain on the market for too long. Buyers who are aware of a long exposure period are often hesitant to make an offer because they fear "something is wrong" with the house. It often happens that homes that are on the market for a long time eventually sell for less than their fair market value.

INCONVENIENCE If overpricing keeps your home from selling promptly, you can end up owning two homes - the one you've already purchased and the one you're trying to sell. This can prove costly and worrisome, as well as inconvenient.

EIGHTY PERCENT OF THE MARKETING OF YOUR HOME IS DONE THE NIGHT WE DECIDE AT WHAT PRICE WE WILL LIST YOUR HOME.

IF YOU ARE UNWILLING TO LIST YOUR HOME AT, OR JUST BELOW, THE

CURRENT MARKET VALUE YOU ARE BETTER SERVED NOT PUTTING IT ON

THE MARKET AT ALL.

FRANK MURPHY

TIME Chances are that your home will sell at its fair market value. Pricing it realistically at the outset simply increases the likelihood of a timely sale with less inconvenience and greater monetary return.

COMPETITION Buyers educate themselves by viewing many homes. They know what is a fair price. If your home is not competitive in value with those they have already seen, it will not sell. Buyers typically look at homes within a $10,000 price range. If your home is not priced within the correct range, it very likely will not be exposed to its potential or targeted buyers.

REPUTATION Overpricing causes most homes to remain on the market for too long. Buyers who are aware of a long exposure period are often hesitant to make an offer because they fear "something is wrong" with the house. It often happens that homes that are on the market for a long time eventually sell for less than their fair market value.

INCONVENIENCE If overpricing keeps your home from selling promptly, you can end up owning two homes - the one you've already purchased and the one you're trying to sell. This can prove costly and worrisome, as well as inconvenient.

EIGHTY PERCENT OF THE MARKETING OF YOUR HOME IS DONE THE NIGHT WE DECIDE AT WHAT PRICE WE WILL LIST YOUR HOME.

IF YOU ARE UNWILLING TO LIST YOUR HOME AT, OR JUST BELOW, THE

CURRENT MARKET VALUE YOU ARE BETTER SERVED NOT PUTTING IT ON

THE MARKET AT ALL.

FRANK MURPHY

Tuesday, September 25, 2007

REVISING MORTGAGE RULES: CAN THERE BE AN AGREEMENT?

With the expectation that hundreds of thousands of homeowners are likely to lose their houses as subprime mortgages are scheduled to raise interest rates over the next 18 months, Democrats propose that "Fannie Mae and Freddie Mac, which guarantee conventional mortgages of up to $417,000, [be allowed to] buy and hold many billions of dollars’ worth of additional mortgages in their own portfolios."

The Bush administration has been, and still remains somewhat, opposed to such a move, reasoning that taxpayers everywhere are put at risk if the investments turn out to be bad for such government-sponsored companies.

To read about how the Bush administration and the Federal Reserve are moving closer to an agreement with House and Senate Democrats regarding this issue, click here.

With the expectation that hundreds of thousands of homeowners are likely to lose their houses as subprime mortgages are scheduled to raise interest rates over the next 18 months, Democrats propose that "Fannie Mae and Freddie Mac, which guarantee conventional mortgages of up to $417,000, [be allowed to] buy and hold many billions of dollars’ worth of additional mortgages in their own portfolios."

The Bush administration has been, and still remains somewhat, opposed to such a move, reasoning that taxpayers everywhere are put at risk if the investments turn out to be bad for such government-sponsored companies.

To read about how the Bush administration and the Federal Reserve are moving closer to an agreement with House and Senate Democrats regarding this issue, click here.

Wednesday, September 19, 2007

FED CUTS RATE; MARKETS SOAR!

Fed cuts prime lending rate by 1/2 % from 5.25% to 4.75% in a dramatic move.

Stock market reacts with large gain.

Impact on mortgage rates and the housing market not clear at this time.

To read the whole article click here.

Fed cuts prime lending rate by 1/2 % from 5.25% to 4.75% in a dramatic move.

Stock market reacts with large gain.

Impact on mortgage rates and the housing market not clear at this time.

To read the whole article click here.

Fed Cuts Rate By Half A Point

by: Vikas Bajaj, NY Times

There was something for just about everyone in the Federal Reserve’s decision yesterday to cut its benchmark interest rate by half a point (from 5.25% to 4.75%).

For homeowners, it could lead to lower mortgage rates in the months to come. For investors, it could help stabilize and bolster volatile share prices. For Wall Street financiers and for companies across America, it could eventually make borrowing easier and cheaper.

“This is a bold move,” said James T. Swanson, chief investment strategist at MFS Investment Management, a mutual fund company in Boston. “It’s going to alleviate concerns that the credit market will kill the economy.”

The rate cut, to 4.75 percent, was twice as large as most investors had expected, and it showed in the market’s reaction. The Standard & Poor’s 500-stock index rose 2.92 percent, to 1,519.78, and the Dow Jones industrial average rose 335.97 points, or 2.51 percent, to 13,739.39. It was the biggest single-day gain for both indexes since early 2003.

Many commercial banks followed the Fed and cut the prime rate they charge their best customers for loans. In the commodity markets, gold and oil prices both surged yesterday afternoon. The dollar fell to a new low against the euro.

Investors in the futures market are now betting that the Fed will cut rates at least once more this year, to 4.5 percent, at the meeting in late October. But the central bank was more guarded. Noting that “some inflation risks remain,” the Fed said that its actions would have to balance concerns about slowing growth against the threat of inflation.

For the broader economy, changes in the Fed’s target short-term interest rate, which banks charge one another, usually takes several months to a year to have a noticeable impact.

The average rate for a 30-year fixed mortgage stood at 6.31 percent last week, down from its high for the year of 6.74 percent in June, Freddie Mac said. The rate could fall further if the Fed’s move and statement encourage investors to buy more mortgage-backed securities, which are used to finance loans.

To read the full article go to: http://www.nytimes.com/2007/09/19/business/19cnd-markets.html?_r=1&adxnnl=1&oref=slogin&adxnnlx=1190223776-8XlJtNOrYT07wNcOxCRmYA

by: Vikas Bajaj, NY Times

There was something for just about everyone in the Federal Reserve’s decision yesterday to cut its benchmark interest rate by half a point (from 5.25% to 4.75%).

For homeowners, it could lead to lower mortgage rates in the months to come. For investors, it could help stabilize and bolster volatile share prices. For Wall Street financiers and for companies across America, it could eventually make borrowing easier and cheaper.

“This is a bold move,” said James T. Swanson, chief investment strategist at MFS Investment Management, a mutual fund company in Boston. “It’s going to alleviate concerns that the credit market will kill the economy.”

The rate cut, to 4.75 percent, was twice as large as most investors had expected, and it showed in the market’s reaction. The Standard & Poor’s 500-stock index rose 2.92 percent, to 1,519.78, and the Dow Jones industrial average rose 335.97 points, or 2.51 percent, to 13,739.39. It was the biggest single-day gain for both indexes since early 2003.

Many commercial banks followed the Fed and cut the prime rate they charge their best customers for loans. In the commodity markets, gold and oil prices both surged yesterday afternoon. The dollar fell to a new low against the euro.

Investors in the futures market are now betting that the Fed will cut rates at least once more this year, to 4.5 percent, at the meeting in late October. But the central bank was more guarded. Noting that “some inflation risks remain,” the Fed said that its actions would have to balance concerns about slowing growth against the threat of inflation.

For the broader economy, changes in the Fed’s target short-term interest rate, which banks charge one another, usually takes several months to a year to have a noticeable impact.

The average rate for a 30-year fixed mortgage stood at 6.31 percent last week, down from its high for the year of 6.74 percent in June, Freddie Mac said. The rate could fall further if the Fed’s move and statement encourage investors to buy more mortgage-backed securities, which are used to finance loans.

To read the full article go to: http://www.nytimes.com/2007/09/19/business/19cnd-markets.html?_r=1&adxnnl=1&oref=slogin&adxnnlx=1190223776-8XlJtNOrYT07wNcOxCRmYA

Monday, September 10, 2007

7 FAST FIXES FOR YOUR CREDIT SCORE

By Liz Pulliam Weston

So you've had a few problems getting the bills paid lately, and you're wondering what you can do to repair the damage.

You've got plenty of company. There are more than 30 million people in the United States with credit blemishes severe enough (and credit scores under 620) to make obtaining loans and credit cards with reasonable terms difficult.

Or maybe your credit is OK, but you'd like to make it better. After all, the better your credit, the lower the interest rates you can secure on mortgages, car loans and credit cards. Know the score In order to improve your credit score, it's important to know where you stand currently. Despite all the media attention given to free credit reports, you still have to pay to find out your credit score, the three-digit number ranging from 300 to 850 that is the key to your borrowing costs. You can obtain your FICO credit scores, the ones lenders use, from MyFico.com. Or you can get Experian's "consumer education" version here.

Now you're ready to take the seven steps to speedy credit repair:

1) Pay down your credit cards. Paying off your installment loans (mortgage, auto, student, etc.) can help your score, but typically not as dramatically as paying down -- or paying off -- revolving accounts like credit cards. The credit-scoring formulas like to see a nice, big gap between the amount of credit you're using and your available credit limits. Getting your balances below 30% of the credit limit on each card can really help. While most debt gurus recommend paying off the highest-rate card first, a better strategy here is to pay down the cards that are closest to their limits.

2) Use your cards lightly. Racking up big balances can hurt your score, regardless of whether you pay your bill in full each month. What's typically reported to the credit bureaus, and thus calculated into your score, is the balance reported on your last statement. (That doesn't mean paying off your balances each month isn't financially smart -- it is -- just that the credit score doesn't care.) You typically can increase your score by limiting your charges to 30% or less of a card's limit. If you're having trouble keeping track, consider using a check register to track your spending, logging into your account frequently at the issuer's Web site, or using personal finance software like Microsoft Money or Quicken, which can download your transactions and balances automatically.

3) Check your limits. Your score might be artificially depressed if your lender is showing a lower limit than you've actually got. Most credit-card issuers will quickly update this information if you ask. If your issuer makes it a policy not to report consumers' limits, however -- as is the usual case with American Express cards and those issued by Capital One -- the bureaus typically use your highest balance as a proxy for your credit limit. You may see the problem here: If you consistently charge the same amount each month -- say $2,000 to $2,500 -- it may look to the credit-scoring formula like you're regularly maxing out that card.You could go on a wild spending spree to raise the limit, but a more sober solution would simply be to pay your balance down or off before your statement period closes. Check your last statement to see which day of the month that typically is, then go to the issuer's Web site about a week in advance of closing and pay off what you owe. It won't raise your reported limit, but it will widen the gap between that limit and your closing balance, which should boost your score.

4) Dust off an old card. The older your credit history, the better. But if you stop using your oldest cards, the issuers may stop updating those accounts at the credit bureaus. The accounts will still appear, but they won't be given as much weight in the credit-scoring formula as your active accounts, said Craig Watts, an executive at Fair Isaac & Co., one of the leading credit scorers. That's why Ferguson often recommends to her clients that they use their oldest cards every few months to charge a small amount, paying it off in full when the statement arrives.

5) Get some goodwill. If you've been a good customer, a lender might agree to simply erase that one late payment from your credit history. You usually have to make the request in writing, and your chances for a "goodwill adjustment" improve the better your record with the company (and the better your credit in general). But it can't hurt to ask. A longer-term solution for more-troubled accounts is to ask that they be "re-aged." If the account is still open, the lender might erase previous delinquencies if you make a series of 12 or so on-time payments.

6) Dispute old negatives. Say that fight with your phone company over an unfair bill a few years ago resulted in a collections account. You can continue protesting that the charge was unjust, or you can try disputing the account with the credit bureaus as "not mine." The older and smaller a collection account, the more likely the collection agency won't bother to verify it when the credit bureau investigates your dispute. Some consumers also have had luck disputing old items with a lender that has merged with another company, which can leave lender records a real mess.

7) Blitz significant errors. Your credit score is calculated based on the information in your credit report, so certain errors there can really cost you. But not everything that's reported in your file matters to your score. Here's the stuff that's usually worth the effort of correcting with the bureaus:

-Late payments, charge-offs, collections or other negative items that aren't yours. -Credit limits reported as lower than they actually are-Accounts listed as "settled," "paid derogatory," "paid charge-off" or anything other than "current" or "paid as agreed" if you paid on time and in full.

-Accounts that are still listed as unpaid that were included in a bankruptcy.

-Negative items older than seven years (10 in the case of bankruptcy) that should have automatically fallen off your report.

You actually have to be a bit careful with this last one, because sometimes scores actually go down when bad items fall off your report. It's a quirk in the FICO credit-scoring software, and the potential effect of eliminating old negative items is difficult to predict in advance.

Some of the stuff that you typically shouldn't worry about includes:

-Various misspellings of your name.

-Outdated or incorrect address information.

-An old employer listed as current.

-Most inquiries.

-If the misspelled name or incorrect address is because of identity theft or because your file has been mixed with someone else's, that should be obvious when you look at your accounts. You'll see delinquencies or accounts that aren't yours and should report that immediately. However, if it's just a goof by the credit bureau or one of the companies reporting to it, it's usually not much to sweat about.

Two more items you don't need to correct:

-Accounts you closed listed as being open.

-Accounts you closed that don't say "closed by consumer." Closing accounts can't help your score, and may hurt it. If your goal is boosting your score, leave these alone. Once an account has been closed, though, it doesn't matter to the scoring formulas who did it -- you or the lender. If you messed up the account, it will be obvious from the late payments and other derogatory information included in the file.

4 other credit mistakes Other actions to beware when you're trying to improve your score:

-Asking a creditor to lower your credit limits. This will reduce that all-important gap between your balances and your available credit, which could hurt your score. If a lender asks you to close an account or get a limit lowered as a condition for getting a loan, you might have to do it -- but don't do so without being asked.

-Making a late payment. The irony here is that a late or missed payment will hurt a good score more than a bad one, dropping a 700-plus score by 100 points or more. If you've already got a string of negative items on your credit report, one more won't have a big impact, but it's still something you want to avoid if you're trying to improve your score.

-Consolidating your accounts. Applying for a new account can ding your score. So, too, can transferring balances from a high-limit card to a lower-limit one, or concentrating all or most of your credit-card balances onto a single card. In general, it's better to have smaller balances on a few cards than a big balance on one.

-Applying for new credit if you've already got plenty. On the other hand, applying for and getting an installment loan can help your score if you don't have any installment accounts, or you're trying to recover from a credit disaster like bankruptcy.

By the way, all these suggestions work best if you have poor or mediocre scores to begin with. Once you've hit the 700 mark, any tweaking you do will tend to have less of a positive impact.And if your scores are in the "excellent" category, 760 or above, you'll probably be able to eke out only a few extra points despite your best efforts. There's really no point, anyway, since you're already qualified for the best rates and terms. Here's one area where it's really OK to rest on your laurels and worry about something else.

Liz Pulliam Weston's column appears every Monday and Thursday, exclusively on MSN Money. She also answers reader questions in the Your Money message board

By Liz Pulliam Weston

So you've had a few problems getting the bills paid lately, and you're wondering what you can do to repair the damage.

You've got plenty of company. There are more than 30 million people in the United States with credit blemishes severe enough (and credit scores under 620) to make obtaining loans and credit cards with reasonable terms difficult.

Or maybe your credit is OK, but you'd like to make it better. After all, the better your credit, the lower the interest rates you can secure on mortgages, car loans and credit cards. Know the score In order to improve your credit score, it's important to know where you stand currently. Despite all the media attention given to free credit reports, you still have to pay to find out your credit score, the three-digit number ranging from 300 to 850 that is the key to your borrowing costs. You can obtain your FICO credit scores, the ones lenders use, from MyFico.com. Or you can get Experian's "consumer education" version here.

Now you're ready to take the seven steps to speedy credit repair:

1) Pay down your credit cards. Paying off your installment loans (mortgage, auto, student, etc.) can help your score, but typically not as dramatically as paying down -- or paying off -- revolving accounts like credit cards. The credit-scoring formulas like to see a nice, big gap between the amount of credit you're using and your available credit limits. Getting your balances below 30% of the credit limit on each card can really help. While most debt gurus recommend paying off the highest-rate card first, a better strategy here is to pay down the cards that are closest to their limits.

2) Use your cards lightly. Racking up big balances can hurt your score, regardless of whether you pay your bill in full each month. What's typically reported to the credit bureaus, and thus calculated into your score, is the balance reported on your last statement. (That doesn't mean paying off your balances each month isn't financially smart -- it is -- just that the credit score doesn't care.) You typically can increase your score by limiting your charges to 30% or less of a card's limit. If you're having trouble keeping track, consider using a check register to track your spending, logging into your account frequently at the issuer's Web site, or using personal finance software like Microsoft Money or Quicken, which can download your transactions and balances automatically.

3) Check your limits. Your score might be artificially depressed if your lender is showing a lower limit than you've actually got. Most credit-card issuers will quickly update this information if you ask. If your issuer makes it a policy not to report consumers' limits, however -- as is the usual case with American Express cards and those issued by Capital One -- the bureaus typically use your highest balance as a proxy for your credit limit. You may see the problem here: If you consistently charge the same amount each month -- say $2,000 to $2,500 -- it may look to the credit-scoring formula like you're regularly maxing out that card.You could go on a wild spending spree to raise the limit, but a more sober solution would simply be to pay your balance down or off before your statement period closes. Check your last statement to see which day of the month that typically is, then go to the issuer's Web site about a week in advance of closing and pay off what you owe. It won't raise your reported limit, but it will widen the gap between that limit and your closing balance, which should boost your score.

4) Dust off an old card. The older your credit history, the better. But if you stop using your oldest cards, the issuers may stop updating those accounts at the credit bureaus. The accounts will still appear, but they won't be given as much weight in the credit-scoring formula as your active accounts, said Craig Watts, an executive at Fair Isaac & Co., one of the leading credit scorers. That's why Ferguson often recommends to her clients that they use their oldest cards every few months to charge a small amount, paying it off in full when the statement arrives.

5) Get some goodwill. If you've been a good customer, a lender might agree to simply erase that one late payment from your credit history. You usually have to make the request in writing, and your chances for a "goodwill adjustment" improve the better your record with the company (and the better your credit in general). But it can't hurt to ask. A longer-term solution for more-troubled accounts is to ask that they be "re-aged." If the account is still open, the lender might erase previous delinquencies if you make a series of 12 or so on-time payments.

6) Dispute old negatives. Say that fight with your phone company over an unfair bill a few years ago resulted in a collections account. You can continue protesting that the charge was unjust, or you can try disputing the account with the credit bureaus as "not mine." The older and smaller a collection account, the more likely the collection agency won't bother to verify it when the credit bureau investigates your dispute. Some consumers also have had luck disputing old items with a lender that has merged with another company, which can leave lender records a real mess.

7) Blitz significant errors. Your credit score is calculated based on the information in your credit report, so certain errors there can really cost you. But not everything that's reported in your file matters to your score. Here's the stuff that's usually worth the effort of correcting with the bureaus:

-Late payments, charge-offs, collections or other negative items that aren't yours. -Credit limits reported as lower than they actually are-Accounts listed as "settled," "paid derogatory," "paid charge-off" or anything other than "current" or "paid as agreed" if you paid on time and in full.

-Accounts that are still listed as unpaid that were included in a bankruptcy.

-Negative items older than seven years (10 in the case of bankruptcy) that should have automatically fallen off your report.

You actually have to be a bit careful with this last one, because sometimes scores actually go down when bad items fall off your report. It's a quirk in the FICO credit-scoring software, and the potential effect of eliminating old negative items is difficult to predict in advance.

Some of the stuff that you typically shouldn't worry about includes:

-Various misspellings of your name.

-Outdated or incorrect address information.

-An old employer listed as current.

-Most inquiries.

-If the misspelled name or incorrect address is because of identity theft or because your file has been mixed with someone else's, that should be obvious when you look at your accounts. You'll see delinquencies or accounts that aren't yours and should report that immediately. However, if it's just a goof by the credit bureau or one of the companies reporting to it, it's usually not much to sweat about.

Two more items you don't need to correct:

-Accounts you closed listed as being open.

-Accounts you closed that don't say "closed by consumer." Closing accounts can't help your score, and may hurt it. If your goal is boosting your score, leave these alone. Once an account has been closed, though, it doesn't matter to the scoring formulas who did it -- you or the lender. If you messed up the account, it will be obvious from the late payments and other derogatory information included in the file.

4 other credit mistakes Other actions to beware when you're trying to improve your score:

-Asking a creditor to lower your credit limits. This will reduce that all-important gap between your balances and your available credit, which could hurt your score. If a lender asks you to close an account or get a limit lowered as a condition for getting a loan, you might have to do it -- but don't do so without being asked.

-Making a late payment. The irony here is that a late or missed payment will hurt a good score more than a bad one, dropping a 700-plus score by 100 points or more. If you've already got a string of negative items on your credit report, one more won't have a big impact, but it's still something you want to avoid if you're trying to improve your score.

-Consolidating your accounts. Applying for a new account can ding your score. So, too, can transferring balances from a high-limit card to a lower-limit one, or concentrating all or most of your credit-card balances onto a single card. In general, it's better to have smaller balances on a few cards than a big balance on one.

-Applying for new credit if you've already got plenty. On the other hand, applying for and getting an installment loan can help your score if you don't have any installment accounts, or you're trying to recover from a credit disaster like bankruptcy.

By the way, all these suggestions work best if you have poor or mediocre scores to begin with. Once you've hit the 700 mark, any tweaking you do will tend to have less of a positive impact.And if your scores are in the "excellent" category, 760 or above, you'll probably be able to eke out only a few extra points despite your best efforts. There's really no point, anyway, since you're already qualified for the best rates and terms. Here's one area where it's really OK to rest on your laurels and worry about something else.

Liz Pulliam Weston's column appears every Monday and Thursday, exclusively on MSN Money. She also answers reader questions in the Your Money message board

Thursday, September 06, 2007

ON PREDICTING THE REAL ESTATE MARKET

Jeff Schoenfield, Frank's colleague and fellow member of the invitation only Allen Hainge CyberStars, offers this opinion about predicting the real estate market. I couldn’t agree more!

"The real question (whether you are a potential buyer or seller) of course is when will the market turn? While I don't have a crystal ball you can be assured of one thing: The turn of the market will NOT be announced by headlines in USA Today and other national and local publications stating 'Real Estate Market Bottom Reached - Now Time to Invest!'. Rather, the news reported will still be mainly negative even as the market turns. We also do know that prices are the best they've been in some time and there are bargains available. By the time the market actually turns and everybody knows about it the best values will be behind us and buyers will have missed their opportunity to get a true bargain."

Jeff Schoenfield

Broker/Owner

RE/MAX All Pro, Realtors, Inc.

Gatlinburg, TN

Jeff@Gatlinburg-Homes.com

Jeff Schoenfield, Frank's colleague and fellow member of the invitation only Allen Hainge CyberStars, offers this opinion about predicting the real estate market. I couldn’t agree more!

"The real question (whether you are a potential buyer or seller) of course is when will the market turn? While I don't have a crystal ball you can be assured of one thing: The turn of the market will NOT be announced by headlines in USA Today and other national and local publications stating 'Real Estate Market Bottom Reached - Now Time to Invest!'. Rather, the news reported will still be mainly negative even as the market turns. We also do know that prices are the best they've been in some time and there are bargains available. By the time the market actually turns and everybody knows about it the best values will be behind us and buyers will have missed their opportunity to get a true bargain."

Jeff Schoenfield

Broker/Owner

RE/MAX All Pro, Realtors, Inc.

Gatlinburg, TN

Jeff@Gatlinburg-Homes.com

Wednesday, September 05, 2007

Show Your Support: Please Join Us in the FLY THE FLAG Campaign

On Tuesday, September 11th, 2007, an American flag should be displayed outside every home, apartment, office, and store in the United States.

Every individual should make it their duty to display an American flag on this sixth anniversary of our country's worst tragedy. We do this in honor of those who lost their lives on 9/11, their families, friends, and loved ones who continue to endure the pain, and those who today are fighting at home and abroad to preserve our cherished freedoms.

In the days, weeks and months following 9/11, our country was bathed in American flags as citizens mourned the incredible losses and stood shoulder-to-shoulder against terrorism. Sadly, those flags have all but disappeared. Our patriotism pulled us through some tough times and it shouldn't take another attack to galvanize us in solidarity. Our American flag is the fabric of our country and together we can prevail over terrorism of all kinds.

Thank you for your participation.

Friday, August 31, 2007

BEN BERNANKE'S SPEECH

JACKSON HOLE, Wyo. -- The Federal Reserve must take the effects of recent financial market disruptions into account in setting monetary policy and is ready to act as needed to ease their impact on the economy, Fed Chairman Ben Bernanke said Friday.

Mr. Bernanke's prepared remarks to the Kansas City Fed's annual Jackson Hole seminar suggest the central bank is set to lower rates unless short-term credit market conditions improve.

"Developments in financial markets can have broad economic effects felt by many outside the markets, and the Federal Reserve must take those effects into account when determining policy," Mr. Bernanke said, The Fed "stands ready to take additional actions" to boost liquidity, "will act as needed to limit the adverse effects on the broader economy that may arise from the disruptions in financial markets."

Mr. Bernanke went further Friday, saying "the further tightening of credit conditions, if sustained, would increase the risk that the current weakness in housing could be deeper or more prolonged than previously expected, with possible adverse effects on consumer spending and the economy more generally." In fact, "global financial losses (triggered largely by subprime mortgage concerns) have far exceeded even the most pessimistic projections of credit losses on those loans," Mr. Bernanke said.

To be sure, Mr. Bernanke's words weren't entirely soothing to investors. "It is not the responsibility of the Federal Reserve -- nor would it be appropriate -- to protect lenders and investors from the consequences of their financial decisions," Mr. Bernanke said.

Still, there was little in Mr. Bernanke's speech that would cause investors to pull back from expectations for reductions in the Fed's primary tool, the federal-funds target rate, which has stood at 5.25% for more than one year. Futures markets are pricing in multiple fed-funds rate cuts by the end of the year.

To read the full article click on this link: http://online.wsj.com/public/article_print/SB118856681612814632.html

JACKSON HOLE, Wyo. -- The Federal Reserve must take the effects of recent financial market disruptions into account in setting monetary policy and is ready to act as needed to ease their impact on the economy, Fed Chairman Ben Bernanke said Friday.

Mr. Bernanke's prepared remarks to the Kansas City Fed's annual Jackson Hole seminar suggest the central bank is set to lower rates unless short-term credit market conditions improve.

"Developments in financial markets can have broad economic effects felt by many outside the markets, and the Federal Reserve must take those effects into account when determining policy," Mr. Bernanke said, The Fed "stands ready to take additional actions" to boost liquidity, "will act as needed to limit the adverse effects on the broader economy that may arise from the disruptions in financial markets."

Mr. Bernanke went further Friday, saying "the further tightening of credit conditions, if sustained, would increase the risk that the current weakness in housing could be deeper or more prolonged than previously expected, with possible adverse effects on consumer spending and the economy more generally." In fact, "global financial losses (triggered largely by subprime mortgage concerns) have far exceeded even the most pessimistic projections of credit losses on those loans," Mr. Bernanke said.

To be sure, Mr. Bernanke's words weren't entirely soothing to investors. "It is not the responsibility of the Federal Reserve -- nor would it be appropriate -- to protect lenders and investors from the consequences of their financial decisions," Mr. Bernanke said.

Still, there was little in Mr. Bernanke's speech that would cause investors to pull back from expectations for reductions in the Fed's primary tool, the federal-funds target rate, which has stood at 5.25% for more than one year. Futures markets are pricing in multiple fed-funds rate cuts by the end of the year.

To read the full article click on this link: http://online.wsj.com/public/article_print/SB118856681612814632.html

BUSH OFFERS RELIEF FOR SOME ON HOME LOANS

WASHINGTON, Aug. 31 — President Bush, in his first response to families hit by the subprime mortgage crisis, announced several steps today to help Americans who have credit problems meet the rising cost of their housing loans. First, to change the federal mortgage insurance program in a way that would let an additional 80,000 homeowners with spotty credit records sign up, beyond the 160,000 likely to use it this year and next. Second, to endorse proposals backed by Democrats in Congress that would raise the ceiling on the amount of a mortgage that can be refinanced with federal insurance and to support legislation that would provide tax breaks to homeowners whose mortgage debt is forgiven, in whole or in part, by lenders.

“It’s not the government’s job to bail out speculators or those who made the decision to buy a home they knew they could never afford,” Mr. Bush said. “Yet there are many American homeowners who can get through this difficult time with a little flexibility from their lenders or little help from their government.”

To read the full article click here: http://www.nytimes.com/2007/08/31/business/31home.html?pagewanted=2&_r=1&th&emc=th

WASHINGTON, Aug. 31 — President Bush, in his first response to families hit by the subprime mortgage crisis, announced several steps today to help Americans who have credit problems meet the rising cost of their housing loans. First, to change the federal mortgage insurance program in a way that would let an additional 80,000 homeowners with spotty credit records sign up, beyond the 160,000 likely to use it this year and next. Second, to endorse proposals backed by Democrats in Congress that would raise the ceiling on the amount of a mortgage that can be refinanced with federal insurance and to support legislation that would provide tax breaks to homeowners whose mortgage debt is forgiven, in whole or in part, by lenders.

“It’s not the government’s job to bail out speculators or those who made the decision to buy a home they knew they could never afford,” Mr. Bush said. “Yet there are many American homeowners who can get through this difficult time with a little flexibility from their lenders or little help from their government.”

To read the full article click here: http://www.nytimes.com/2007/08/31/business/31home.html?pagewanted=2&_r=1&th&emc=th

Monday, August 20, 2007

FED CUTS DISCOUNT RATE, ADMITS CONCERN

Last Friday the Fed, acknowledging for the first time "the risk of an economic downturn," cut its discount rate from 6.25% to 5.75%, "encouraging the nation’s banks to borrow directly from the Fed." Following the announcement, the Dow Jones changed direction and shot up 1.8 percent on Friday morning.

The move came at the realization that even creditworthy homebuyers are now having trouble obtaining mortgages, and is particularly notable given that "the Fed’s standard practice, for more than a decade, has been to change rates and issue statements only at scheduled meetings of policy makers." But as the stock market continues to falter, the Fed's chairman Ben Bernanke scheduled a conference call during which the policy makers voted unanimously on the lowered discount rate.

While the cut signals that even the Fed has found it necessary to admit economic fears, at the consumer level, it seems people--for the moment--are more frustrated with the high prices of food and gas than they are suffering from a dread of economic crises, according to a recent study done by the University of Michigan.

To read the New York Times article in its entirety, go to Fearing Slide in the Economy, Fed Cuts Its Discount Rate

Last Friday the Fed, acknowledging for the first time "the risk of an economic downturn," cut its discount rate from 6.25% to 5.75%, "encouraging the nation’s banks to borrow directly from the Fed." Following the announcement, the Dow Jones changed direction and shot up 1.8 percent on Friday morning.

The move came at the realization that even creditworthy homebuyers are now having trouble obtaining mortgages, and is particularly notable given that "the Fed’s standard practice, for more than a decade, has been to change rates and issue statements only at scheduled meetings of policy makers." But as the stock market continues to falter, the Fed's chairman Ben Bernanke scheduled a conference call during which the policy makers voted unanimously on the lowered discount rate.

While the cut signals that even the Fed has found it necessary to admit economic fears, at the consumer level, it seems people--for the moment--are more frustrated with the high prices of food and gas than they are suffering from a dread of economic crises, according to a recent study done by the University of Michigan.

To read the New York Times article in its entirety, go to Fearing Slide in the Economy, Fed Cuts Its Discount Rate

Monday, August 13, 2007

"THE MORTGAGE MAZE"

Perhaps you've heard of "securitization"? It goes something like this: "The process begins with the entity that originates the loan, either a mortgage broker or lender. The loan is assigned to a company that will service it — collecting borrowers’ payments and distributing them to investors. Sometimes the servicer is affiliated with the lender, creating potential conflicts if a loan goes bad. A Wall Street firm then pools thousands of loans to be sold to investors who want a steady stream of cash from loan payments. The underwriters separate them into segments based on risk. Once a trust is sold, a trustee bank oversees its operations on behalf of investors. The trustee makes sure that the terms of the pooling and servicing agreement are met; this document determines what a servicer can do to help distressed borrowers."

Maybe this is why so many distressed borrowers are finding it so difficult to get loan modifications, or even figure out simply who holds the mortgages. Dianne Brimmage of Alton, IL, refinanced her home's mortgage (the home she has lived in since 1998) in order to consolidate car and medical bills. Now she struggles with a high interest rate and would like to modify the terms of her loan.

Though in the past this might have been easy to do because it was in every one's best interest, the only concern now is making a profit and there are so many different parties involved in the mortgage process that each one can deny information and manage to put off a solution that is helpful to the homeowner indefinitely.

To read the article in its entirety, go to "The Mortgage Maze May Increase Foreclosures"

Perhaps you've heard of "securitization"? It goes something like this: "The process begins with the entity that originates the loan, either a mortgage broker or lender. The loan is assigned to a company that will service it — collecting borrowers’ payments and distributing them to investors. Sometimes the servicer is affiliated with the lender, creating potential conflicts if a loan goes bad. A Wall Street firm then pools thousands of loans to be sold to investors who want a steady stream of cash from loan payments. The underwriters separate them into segments based on risk. Once a trust is sold, a trustee bank oversees its operations on behalf of investors. The trustee makes sure that the terms of the pooling and servicing agreement are met; this document determines what a servicer can do to help distressed borrowers."

Maybe this is why so many distressed borrowers are finding it so difficult to get loan modifications, or even figure out simply who holds the mortgages. Dianne Brimmage of Alton, IL, refinanced her home's mortgage (the home she has lived in since 1998) in order to consolidate car and medical bills. Now she struggles with a high interest rate and would like to modify the terms of her loan.

Though in the past this might have been easy to do because it was in every one's best interest, the only concern now is making a profit and there are so many different parties involved in the mortgage process that each one can deny information and manage to put off a solution that is helpful to the homeowner indefinitely.

To read the article in its entirety, go to "The Mortgage Maze May Increase Foreclosures"

Tuesday, August 07, 2007

ADDICTED TO ONLINE REAL ESTATE INFORMATION?

Well, you're not alone. According to The New York Times' Michelle Slatalla, "in June... more than 39 million people visited the 20 most popular real estate Web sites, a 22.4 percent increase in visitors over the same period in the previous year, according to Nielsen/NetRatings Inc. Not only that, but a lot of those people are becoming addicted. At Zillow.com, for instance, 44 percent of the site’s users visited five or more times in June, and 25 percent of them 10 or more times, according to a spokeswoman for the site."

Unfortunately, the information one can glean from these sites often seems so contradictory that it's hardly worth the emotional stress or rash decisions that can be triggered by the numbers. For example, the difference between the highest and lowest values of Ms. Slatalla's home as stated by two different appraisal sites was $699,974. On top of that, when a real-life appraiser came to see her home he quoted her a value that was "$100,000 more than the highest online estimate."

So don't be sucked into the check-your-neighbor's-home-value-every-five-minutes spiral; and if you can't help yourself, remember to take it all with a grain of salt.

For a thoughtful, reliable, in-person estimate of your home's current market value, please email me, or give me a call at 831-457-5550.

To read Ms. Slatalla's article in its entirety, go to What's My House Worth? And Now...?

Well, you're not alone. According to The New York Times' Michelle Slatalla, "in June... more than 39 million people visited the 20 most popular real estate Web sites, a 22.4 percent increase in visitors over the same period in the previous year, according to Nielsen/NetRatings Inc. Not only that, but a lot of those people are becoming addicted. At Zillow.com, for instance, 44 percent of the site’s users visited five or more times in June, and 25 percent of them 10 or more times, according to a spokeswoman for the site."

Unfortunately, the information one can glean from these sites often seems so contradictory that it's hardly worth the emotional stress or rash decisions that can be triggered by the numbers. For example, the difference between the highest and lowest values of Ms. Slatalla's home as stated by two different appraisal sites was $699,974. On top of that, when a real-life appraiser came to see her home he quoted her a value that was "$100,000 more than the highest online estimate."

So don't be sucked into the check-your-neighbor's-home-value-every-five-minutes spiral; and if you can't help yourself, remember to take it all with a grain of salt.

For a thoughtful, reliable, in-person estimate of your home's current market value, please email me, or give me a call at 831-457-5550.

To read Ms. Slatalla's article in its entirety, go to What's My House Worth? And Now...?

Monday, July 30, 2007

COUNTRYWIDE ACKNOWLEDGES HOUSING MARKET WOES

On July 24th Countrywide Financial acknowledged that the housing market "might not begin recovering until 2009 because of a decline in house prices," and that even borrowers with good credit are starting to fall behind on their loans. This announcement triggered a sell-off in the stock market, and signals a shift toward a more skeptical view of the future of the housing market than that to which many executives have previously held. According to Vikas Bajaj of the New York Times, Angelo Mozilo, Countrywide's chairman and chief executive, said that "because of a large number of homes on the market, the housing sector would continue to suffer until sometime in 2008 and not begin recovering until 2009."

As a result of the downturn, major lenders such as Countrywide, Wells Fargo, and others have stopped offering risky sub-prime mortgages. But it isn't just sub-prime borrowers who are struggling with payments. Even "credit-worthy" customers are showing the potential to default as home prices fall. "Countrywide said about 5.4 percent of the home equity loans to customers with good credit that it held an interest in were past due at the end of June, up from 2.2 percent at the end of June 2006."

To read the article in its entirety and see detailed statistics, go to Top Lender Sees Mortgage Woes for ‘Good’ Risks

On July 24th Countrywide Financial acknowledged that the housing market "might not begin recovering until 2009 because of a decline in house prices," and that even borrowers with good credit are starting to fall behind on their loans. This announcement triggered a sell-off in the stock market, and signals a shift toward a more skeptical view of the future of the housing market than that to which many executives have previously held. According to Vikas Bajaj of the New York Times, Angelo Mozilo, Countrywide's chairman and chief executive, said that "because of a large number of homes on the market, the housing sector would continue to suffer until sometime in 2008 and not begin recovering until 2009."

As a result of the downturn, major lenders such as Countrywide, Wells Fargo, and others have stopped offering risky sub-prime mortgages. But it isn't just sub-prime borrowers who are struggling with payments. Even "credit-worthy" customers are showing the potential to default as home prices fall. "Countrywide said about 5.4 percent of the home equity loans to customers with good credit that it held an interest in were past due at the end of June, up from 2.2 percent at the end of June 2006."

To read the article in its entirety and see detailed statistics, go to Top Lender Sees Mortgage Woes for ‘Good’ Risks

Monday, July 23, 2007

LIBRARIES OF THE MASTERS

Harriet Rubin's recent article in the New York Times, entitled "C.E.O. Libraries Reveal Keys to Success," provides a fascinating glimpse into the sources of inspiration and wisdom for some of the most successful and innovative business persons of our time.

From Nike founder Phil Knight to Apple's Steven Jobs to Visa founder Dee Hock, it turns out that personal--and often very private--libraries seem to be the most valuable of treasures for these giants.

The libraries that Rubin's investigated combine to create quite the eclectic collection: Asian history, Aristotle, William Blake, T. E. Lawrence, Machiavelli, John Steinbeck, Omar Khayyam, and John Cornwall, just to name a few.

In addition to the most well known writers and thinkers throughout history, many of the articles featured librarians keep every book they've ever read. As Shelly Lazarus, the chairwoman and chief executive of Ogilvy & Mather, says: "Once I’ve read a book I keep it. It becomes a part of me."

To read the article in its entirety, go to "C.E.O. Libraries Reveal Keys to Success "

Harriet Rubin's recent article in the New York Times, entitled "C.E.O. Libraries Reveal Keys to Success," provides a fascinating glimpse into the sources of inspiration and wisdom for some of the most successful and innovative business persons of our time.

From Nike founder Phil Knight to Apple's Steven Jobs to Visa founder Dee Hock, it turns out that personal--and often very private--libraries seem to be the most valuable of treasures for these giants.

The libraries that Rubin's investigated combine to create quite the eclectic collection: Asian history, Aristotle, William Blake, T. E. Lawrence, Machiavelli, John Steinbeck, Omar Khayyam, and John Cornwall, just to name a few.

In addition to the most well known writers and thinkers throughout history, many of the articles featured librarians keep every book they've ever read. As Shelly Lazarus, the chairwoman and chief executive of Ogilvy & Mather, says: "Once I’ve read a book I keep it. It becomes a part of me."

To read the article in its entirety, go to "C.E.O. Libraries Reveal Keys to Success "

Monday, July 02, 2007

ONLY BILLIONAIRES NEED APPLY...

With 56,000 square feet, 95 acres, and a price tag of $135 million, Hala Ranch in Aspen, Colorado is the most expensive single-family residential property in the nation on the market, according to Kirk Johnson of the New York Times.

The property was built for the family of Prince Bandar bin Sultan who served as the ambassador to the United States for Saudi Arabia until 2005. Prince Bandar now works for the Saudi National Security Council and is selling the property as he will not be spending as much time in the States.

"Mere wealth" cannot afford the luxuries of Hala (the private barbershop and beauty salon just off the master suite, for example); Joshua Saslove, the real estate broker who's listing the property, will only consider billionaires. Since there are only 946 billionaires out there, according to Forbes, the pickings are rather slim.

But such is the story of Aspen's west side, where "an ordinary lot, 60 feet by 100 feet, costs $3.5 million."

To read the article in its entirety, go to "A $135 Million Home, but if You Have to Ask ..."

With 56,000 square feet, 95 acres, and a price tag of $135 million, Hala Ranch in Aspen, Colorado is the most expensive single-family residential property in the nation on the market, according to Kirk Johnson of the New York Times.

The property was built for the family of Prince Bandar bin Sultan who served as the ambassador to the United States for Saudi Arabia until 2005. Prince Bandar now works for the Saudi National Security Council and is selling the property as he will not be spending as much time in the States.

"Mere wealth" cannot afford the luxuries of Hala (the private barbershop and beauty salon just off the master suite, for example); Joshua Saslove, the real estate broker who's listing the property, will only consider billionaires. Since there are only 946 billionaires out there, according to Forbes, the pickings are rather slim.

But such is the story of Aspen's west side, where "an ordinary lot, 60 feet by 100 feet, costs $3.5 million."

To read the article in its entirety, go to "A $135 Million Home, but if You Have to Ask ..."

Tuesday, June 12, 2007

HOPEFUL FED WON'T CUT RATES

The Dow Jones fell more than 80 points on June 5th after a widespread realization that there is "almost no chance" that the Fed will cut interest rates by the end of the year.

The Fed chairman, Ben Bernanke, said "that the Fed expected the economy to pull out of its current funk and weather the slowdown in the housing market."

While investors have recently been expecting a rate cut by the end of the year, leading economists are noting that the slowly strengthening economy gives the Fed little reason to buffer against "a worse-than-expected slowdown" for now.

To read Jeremy Peters' article in its entirety, go to Fed Dims Hopes For A Rate Cut

The Dow Jones fell more than 80 points on June 5th after a widespread realization that there is "almost no chance" that the Fed will cut interest rates by the end of the year.

The Fed chairman, Ben Bernanke, said "that the Fed expected the economy to pull out of its current funk and weather the slowdown in the housing market."

While investors have recently been expecting a rate cut by the end of the year, leading economists are noting that the slowly strengthening economy gives the Fed little reason to buffer against "a worse-than-expected slowdown" for now.

To read Jeremy Peters' article in its entirety, go to Fed Dims Hopes For A Rate Cut

Monday, June 04, 2007

THE NEW WAVE OF ONLINE REAL ESTATE

"What we’ve wanted to do, quietly, is amass the largest real estate position on the Internet...." Such is the ambition of Kelly P. Conlin, the chief executive of NameMedia, "a privately held owner and developer of Web sites based in Waltham, Massachusetts."

NameMedia represents the largest and latest success in the area of what Bob Tedeschi of the New York Times calls "online property development." The company owns 725,000 websites and gets its business from the 5-10% of Internet users who use direct navigation (typing in the hypothetical name of a website based on what they're looking to find) rather than search engines.

NameMedia either develops the content of more profitable domain names to include information that users are looking for, or fills the sites with search engine ads and receives a commission from the engines when someone clicks on a link. Independent website owners also add their sites to NameMedia's network, producing even more revenue for the company based on carefully chosen ads placed on those sites.

NameMedia's business represents a new wave in Internet investment, and remains at the forefront of its field. After all, web publishers are always more than happy to expose their content to as many people as possible and make more money in the process.

To read Bob Tedeschi's article in its entirety, go to Millions of Addresses and Thousands of Sites

"What we’ve wanted to do, quietly, is amass the largest real estate position on the Internet...." Such is the ambition of Kelly P. Conlin, the chief executive of NameMedia, "a privately held owner and developer of Web sites based in Waltham, Massachusetts."

NameMedia represents the largest and latest success in the area of what Bob Tedeschi of the New York Times calls "online property development." The company owns 725,000 websites and gets its business from the 5-10% of Internet users who use direct navigation (typing in the hypothetical name of a website based on what they're looking to find) rather than search engines.

NameMedia either develops the content of more profitable domain names to include information that users are looking for, or fills the sites with search engine ads and receives a commission from the engines when someone clicks on a link. Independent website owners also add their sites to NameMedia's network, producing even more revenue for the company based on carefully chosen ads placed on those sites.

NameMedia's business represents a new wave in Internet investment, and remains at the forefront of its field. After all, web publishers are always more than happy to expose their content to as many people as possible and make more money in the process.

To read Bob Tedeschi's article in its entirety, go to Millions of Addresses and Thousands of Sites

Tuesday, May 29, 2007

EFFECTIVE REAL ESTATE SALES FOR WEB 2.0

Reality Magazine recently published an article describing the benefits of a group to which I belong called the Allen F. Hainge CyberStars. CyberStars includes 201 Realtors, both here in the States and abroad, who are at the top of their market and interested in conversing about the very latest technology that will help sell homes for the most amount of money in the least amount of time.

In the midst of Web 2.0--"the Internet’s progression of social-networking and media-sharing sites"--staying web-savvy for a Realtor no longer means simply having a website. Allen Hainge and his group are committed to finding the latest "technology tools," including the incorporation of digital video, podcasts, blogs and MySpace pages.

Because my fellow CyberStar members are "market leaders—the higher-power group" who are necessarily willing "to share ideas on how technology increases profit, and how we can make our Web sites better to contact buyers and sellers," my clients are truly the ones who benefit from this association.

To read more about how CyberStars got started and hear what other members have to say about the group, go to Techie Supernovae Explode in Real Estate Market

To take a look at my own website, go to www.LiveInSantaCruz.com

Reality Magazine recently published an article describing the benefits of a group to which I belong called the Allen F. Hainge CyberStars. CyberStars includes 201 Realtors, both here in the States and abroad, who are at the top of their market and interested in conversing about the very latest technology that will help sell homes for the most amount of money in the least amount of time.

In the midst of Web 2.0--"the Internet’s progression of social-networking and media-sharing sites"--staying web-savvy for a Realtor no longer means simply having a website. Allen Hainge and his group are committed to finding the latest "technology tools," including the incorporation of digital video, podcasts, blogs and MySpace pages.

Because my fellow CyberStar members are "market leaders—the higher-power group" who are necessarily willing "to share ideas on how technology increases profit, and how we can make our Web sites better to contact buyers and sellers," my clients are truly the ones who benefit from this association.

To read more about how CyberStars got started and hear what other members have to say about the group, go to Techie Supernovae Explode in Real Estate Market

To take a look at my own website, go to www.LiveInSantaCruz.com

Monday, May 21, 2007